The research and analysis of the EBITDA indicator are relevant in modern economics and business. This article will explain the essence and value of this indicator.

What is EBITDA?

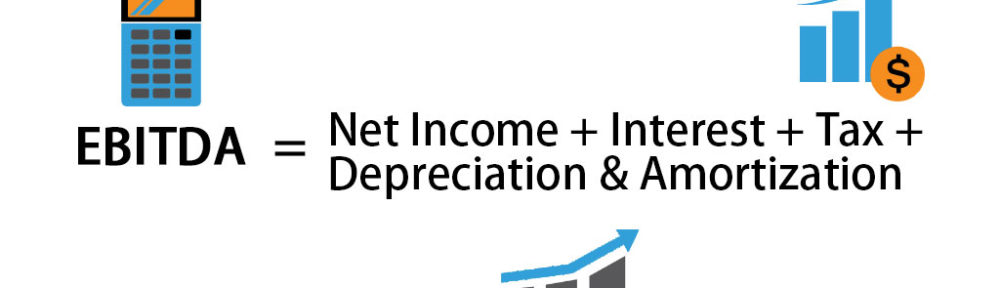

Today, analytical indicators such as EBITDA and OIBDA are used to assess the effectiveness of the enterprise in general and operating activities in particular, as well as to calculate several other indicators: return on assets, coverage ratio interest, return on equity, break-even point, etc. EBITDA (Earnings before interest, taxes, depreciation, and depreciation) – an analytical indicator equal to the amount of profit before deducting the cost of interest, taxes, and accrued depreciation.

EBITDA first gained popularity in the mid-1980s and was used to determine a company’s ability to service debt. This indicator, combined with the net profit indicator, served as a source of information about the number of interest payments the company can provide soon. EBITDA was primarily used by investors who viewed the company not as a long-term investment but as a set of assets that could be profitably sold separately, with indicators characterizing the amount that could be used to repay loans.

In general, EBITDA reflects the income received by the enterprise from operating activities. It does not take into account:

- the amount of investment in production (adjustment for the amount of accrued depreciation);

- debt burden (interest adjustment);

- tax regime (adjustment for income tax).

EBITDA is one of the most widely used analytical indicators in assessing business efficiency, which allows you to compare the financial performance of different companies operating in the same industry and engaged in the same activity. This indicator is of particular importance for characterizing the efficiency of enterprises with a high level of depreciation in total costs.

How to calculate EBITDA?

Typically, EBITDA is calculated by adjusting the company’s net profit by interest receivable/ payable, income tax, depreciation, and other non-operating income and expenses. Still, there is a second option for calculating this indicator.

There are many examples of bankruptcies of companies whose managers mistakenly or maliciously embellished financial results based on EBITDA. Therefore, using this indicator, we must not forget that depreciation reflects the need to upgrade production assets. If we consider EBITDA in terms of its usefulness, we note that it is necessary primarily for external consumers of information: investors, analysts, and all those who want to compare one company with others working in the same field. The indicator margin is one of the main criteria by which companies can be compared. From this point of view, this indicator will help assess their own business and internal consumers of information: financial managers, managers, and shareholders of the analyzed organizations.

The primary purpose of EBITDA is to compare different companies operating in the same industry. The size of the investment or the tax regime applied does not matter; only the type of activity and operating results are essential. Thus, EBITDA allows you to compare companies with different accounting policies (for example, depreciation or asset revaluation), other tax conditions, or the level of debt burden.

The indicator is calculated based on the company’s financial statements and is used to assess the company’s profitability without depreciation. The indicator is used when comparing with industry counterparts, which allows you to determine the effectiveness of the company regardless of its debt to various creditors and the state, as well as the method of depreciation. The indicator is not part of accounting standards. They were originally intended to analyze the attractiveness of takeover agreements on borrowed funds.